KITA 경제정보

[KOCHAM] 주간경제(BOK) , COVID-19 여파 전망(JP모건)

작성자

kita master

작성일

2020-04-11 10:04

조회

19796

안녕하십니까?

KOCHAM 사무국입니다.

금일은 아래 두개 보내드립니다.

※JP 모건 경제자료를 코참이 계속 받기 위해서는, 해당 자료를 외부에 노출하지 마시고 내부용도로만 활용바랍니다.※

모두 건강하시길 바라며 좋은 주말 보내시기 바랍니다.

감사합니다.

사무국 드림

[국제 금융시장 동향]

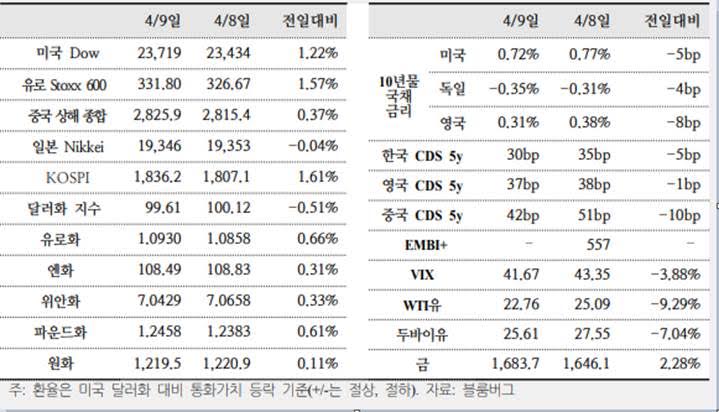

[주가*] 미국 다우지수와 유럽 Stoxx 600 지수는 1.2%, 1.6% 상승

*미국 연준의 기업 및 지방정부 지원 대책이 호재로 반영

[환율*] 달러화 지수는 0.5% 하락. 유로화와 엔화의 가치는 각각 0.7%, 0.3% 상승

*외환시장에서는 연준의 긴급 지원책으로 안전자산인 미국 달러화 수요가 저하

[금리*] 주요국 10년물 국채 금리는 모두 하락

*미국은 연준의 통화정책 완화 장기화 시사 등으로 채권매수가 확대

[주요국 동향 및 경제관련 소식]

[미국] 미국연준, 중소기업 등에 2조3천억달러의긴급지원책발표

연준 파월 의장은 신용 흐름을 지원하기 위해 시행하고 있는 대책의 대부분은

긴급대출 권한에 의존하고 있는 것이라고 언급. 아울러 시장이 중요한 기능을

다시 수행하는 시점까지 연준은 긴급조치를 유지한다고 표명

이러한 가운데 연준은 코로나 19 대응의 일환으로 지방정부 외에 중소기업 등에

2조3천억달러의 지원책을 발표. 구체적으로 종업원 수 1만명 이하의 기업에게

4년간 대출을 민간은행에서 시행하고, 지방정부의 발행채권을 매입

[중국] 중국 자동차 시장, 코로나 19 여파에서 점차 회복

국가발전개혁위원회의 차이룽화(蔡榮華), 2월 자동차 판매 감소는 일시적이며,

자국 자동차업계의 장기 추세에 영향을 미치지 않는다고 주장. 또한 현 시점에서

자동차 생산은 공급장애 여파가 없다고 부연

[해외시각 및 시장평가]

-연준의 자산매입대상확대, 금융시장 안정과 자산가격왜곡의 장단점 혼재 – Financial Times

-미국의 코로나19에 의한 일자리 감소, 경제적 여파로 장기간 지속 될 전망- WSJ

-이탈리아의 부채위기, ECB·E의 지원 등으로 문제해결가능- 블룸버그

[환율 정보]

미국 외환시장 환율

[기준일시: 2020년 04월10일]

아래는 JP모건 경제 자료입니다. (자세한건 파란색 글씨를 클릭하세요)

The Long-term Strategist: Some Longer-term Consequences of Covid-19 Crisis, Jan Loeys

The speed, breadth, and depth of the COVID-19 crash should raise savings rates and risk premia. Social distancing (SD) will largely fade, as people are social animals. Working from home is not as productive. But some SD will stay. Expect more online everything, aversion to crowded places, and more personal vs. public transportation. Companies will focus on building resilience, diversifying supply chains, reducing leverage and short-dated funding, improving liquidity, and adding online services. Global crises demand global cooperation and thus offer an opportunity to bring the world together. So far, we see more go-it-alone and close-the-border politics, adding to de-globalization. The perceived lack of solidarity between Northern and Southern EU again threatens EU cohesiveness, but will likely force another step towards a fiscal union. Building resilience, higher business concentration, a greater role for government and a greater need for distance should do long-term damage to productivity, even as human ingenuity will find ways to adapt and reverse some of this damage. The massive cost of saving lives and jobs will likely move the battle on Climate Change to the back burner for 1-2 years. Recession fast-forwarded our zero-US-yield scenario. Pandemics have historically pushed real rates down as people save more. Inflation will fall badly over the next 1-2 years, keeping monetary policy super-easy. But the blurring of the line between monetary and fiscal authorities raises the risk that the narrative will switch to debt monetization, higher inflation expectations, and higher nominal yields. Asset repricing greatly improves long-term expected returns on equities and credit, while worsening returns on government debt.

US: It starts with an unemployment earthquake, Michael Feroli, Jesse Edgerton, Daniel Silver

Over the last three weeks jobless claims have cumulated to 16.8 million. With these data in hand we think the April jobs report could indicate about 25 million jobs lost since the March survey week, and an unemployment rate around 20% (our final estimates will be refined later in the month). Given the expected hit to hours worked this quarter we now look for -40.0% annualized real GDP growth in 2Q, down from -25.0% previously. We continue to expect a 2H growth recovery, under the strong assumption that virus disruptions fade by June. The long-run destruction to the level of output is difficult to quantify, but likely quite large.

KOCHAM 사무국입니다.

금일은 아래 두개 보내드립니다.

- [신한은행 아메리카]의 경제정보 (추가 첨부파일)

- JP 모건에서 보내온 COVID-19 여파 전망에 대한 글 (링크 첨부) 를 보내드립니다.

※JP 모건 경제자료를 코참이 계속 받기 위해서는, 해당 자료를 외부에 노출하지 마시고 내부용도로만 활용바랍니다.※

모두 건강하시길 바라며 좋은 주말 보내시기 바랍니다.

감사합니다.

사무국 드림

[국제 금융시장 동향]

[주가*] 미국 다우지수와 유럽 Stoxx 600 지수는 1.2%, 1.6% 상승

*미국 연준의 기업 및 지방정부 지원 대책이 호재로 반영

[환율*] 달러화 지수는 0.5% 하락. 유로화와 엔화의 가치는 각각 0.7%, 0.3% 상승

*외환시장에서는 연준의 긴급 지원책으로 안전자산인 미국 달러화 수요가 저하

[금리*] 주요국 10년물 국채 금리는 모두 하락

*미국은 연준의 통화정책 완화 장기화 시사 등으로 채권매수가 확대

[주요국 동향 및 경제관련 소식]

[미국] 미국연준, 중소기업 등에 2조3천억달러의긴급지원책발표

연준 파월 의장은 신용 흐름을 지원하기 위해 시행하고 있는 대책의 대부분은

긴급대출 권한에 의존하고 있는 것이라고 언급. 아울러 시장이 중요한 기능을

다시 수행하는 시점까지 연준은 긴급조치를 유지한다고 표명

이러한 가운데 연준은 코로나 19 대응의 일환으로 지방정부 외에 중소기업 등에

2조3천억달러의 지원책을 발표. 구체적으로 종업원 수 1만명 이하의 기업에게

4년간 대출을 민간은행에서 시행하고, 지방정부의 발행채권을 매입

[중국] 중국 자동차 시장, 코로나 19 여파에서 점차 회복

국가발전개혁위원회의 차이룽화(蔡榮華), 2월 자동차 판매 감소는 일시적이며,

자국 자동차업계의 장기 추세에 영향을 미치지 않는다고 주장. 또한 현 시점에서

자동차 생산은 공급장애 여파가 없다고 부연

[해외시각 및 시장평가]

-연준의 자산매입대상확대, 금융시장 안정과 자산가격왜곡의 장단점 혼재 – Financial Times

-미국의 코로나19에 의한 일자리 감소, 경제적 여파로 장기간 지속 될 전망- WSJ

-이탈리아의 부채위기, ECB·E의 지원 등으로 문제해결가능- 블룸버그

[환율 정보]

미국 외환시장 환율

[기준일시: 2020년 04월10일]

아래는 JP모건 경제 자료입니다. (자세한건 파란색 글씨를 클릭하세요)

The Long-term Strategist: Some Longer-term Consequences of Covid-19 Crisis, Jan Loeys

The speed, breadth, and depth of the COVID-19 crash should raise savings rates and risk premia. Social distancing (SD) will largely fade, as people are social animals. Working from home is not as productive. But some SD will stay. Expect more online everything, aversion to crowded places, and more personal vs. public transportation. Companies will focus on building resilience, diversifying supply chains, reducing leverage and short-dated funding, improving liquidity, and adding online services. Global crises demand global cooperation and thus offer an opportunity to bring the world together. So far, we see more go-it-alone and close-the-border politics, adding to de-globalization. The perceived lack of solidarity between Northern and Southern EU again threatens EU cohesiveness, but will likely force another step towards a fiscal union. Building resilience, higher business concentration, a greater role for government and a greater need for distance should do long-term damage to productivity, even as human ingenuity will find ways to adapt and reverse some of this damage. The massive cost of saving lives and jobs will likely move the battle on Climate Change to the back burner for 1-2 years. Recession fast-forwarded our zero-US-yield scenario. Pandemics have historically pushed real rates down as people save more. Inflation will fall badly over the next 1-2 years, keeping monetary policy super-easy. But the blurring of the line between monetary and fiscal authorities raises the risk that the narrative will switch to debt monetization, higher inflation expectations, and higher nominal yields. Asset repricing greatly improves long-term expected returns on equities and credit, while worsening returns on government debt.

US: It starts with an unemployment earthquake, Michael Feroli, Jesse Edgerton, Daniel Silver

Over the last three weeks jobless claims have cumulated to 16.8 million. With these data in hand we think the April jobs report could indicate about 25 million jobs lost since the March survey week, and an unemployment rate around 20% (our final estimates will be refined later in the month). Given the expected hit to hours worked this quarter we now look for -40.0% annualized real GDP growth in 2Q, down from -25.0% previously. We continue to expect a 2H growth recovery, under the strong assumption that virus disruptions fade by June. The long-run destruction to the level of output is difficult to quantify, but likely quite large.